Read Time:

4-minute

article

Rethinking risk tolerance

This content is categorized as:

Many working-age adults rely on 401(k)s, IRAs and other individual investment accounts to help build retirement savings and pursue long-term growth. While these accounts can be powerful tools to help build a nest egg, creating a comprehensive retirement plan that also includes guaranteed income solutions may help provide financial security for the future.

As you move through different stages of life, your priorities around growth, income and protection often shift, especially as you near retirement. This can be a good time to take a fresh look at your risk tolerance and help ensure your retirement strategy aligns with your goals and vision for the future.

Why risk tolerance can change near retirement

Your risk tolerance can evolve over time as your financial situation and priorities change. In earlier stages of saving, there is often more time to ride out market fluctuations, which can make a growth-focused approach feel more comfortable. But as retirement gets closer, the focus can shift toward turning savings into dependable income and protecting the lifestyle you want for the future.

This shift doesn’t necessarily mean moving away from growth, but rebalancing priorities within a broader retirement strategy.

What might your risk tolerance look like now? Take this quick quiz to help you gain a better understanding of your preferences and expectations as you evaluate retirement planning strategies.

What’s your risk tolerance?

Learning how you feel about investing and saving for the future can allow you to create a financial strategy that helps support your retirement goals.

This quick quiz can help you gain a better understanding of your tolerance for financial risk.

Balancing growth and protection in retirement planning

Creating a retirement strategy isn’t about choosing between growth and security, but finding the right balance between the two. Reducing your exposure to volatile markets and locking in some income guarantees may help you feel more confident about staying on track for the long term.

Annuities can help. Two strategies that can be part of a balanced approach include:

| Strategy |

How it may help |

| Allocate a portion of savings to fixed rate products like multi-year guarantee annuities |

Can help provide more stability and reduce overall portfolio volatility. |

| Use annuities for guaranteed income in retirement |

Can create a "retirement paycheck" you can't outlive |

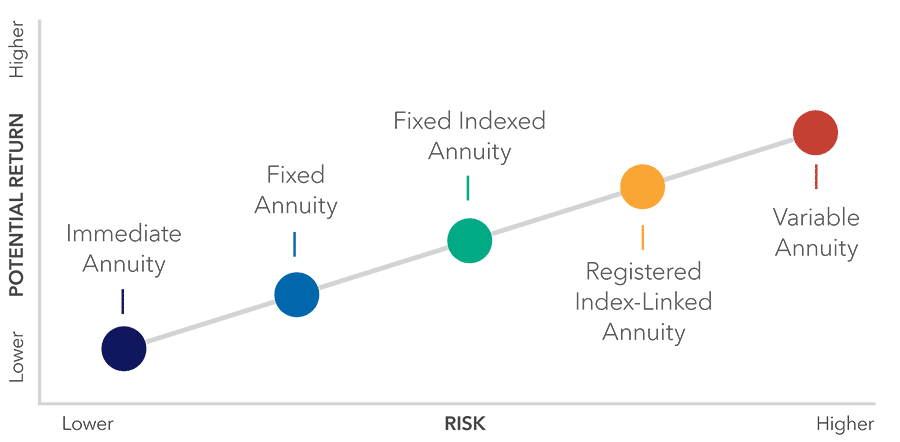

Understanding the annuity risk spectrum

Annuities are designed to help you achieve your retirement savings goals and provide future income. By helping insulate you from major financial risks like stock market losses or outliving your money, they could be part of a solution that helps you stay in your financial comfort zone.

In this chart, you’ll see how different kinds of annuities are mapped along a risk spectrum. The left side of the spectrum is the most conservative. Someone with the highest tolerance for risk may feel comfortable at the far right.

Matching retirement solutions to financial goals

While all annuities are designed to provide income for retirement, there are different kinds to align with your accumulation goals and how much risk you’re comfortable taking.

| Annuity type |

Risk profile |

How it works |

| Immediate annuity |

Lower level of risk |

Converts your premium payment to a guaranteed income stream for life, or for a specific period. |

| Fixed annuity |

Lower risk with guaranteed interest |

Offers a fixed interest rate that’s guaranteed for a certain time period. The guarantee may appeal to you if you’re willing to give up some growth potential if the markets rise. |

| Fixed indexed annuity |

Moderate risk |

You can earn interest based in part on the upward movement of a stock market index while enjoying the protection of a zero percent floor. If the net change in the index over a given crediting period is negative, you would earn zero interest for that period, but never less than zero. |

| Registered index-linked annuity |

Higher risk tolerance |

Offers the potential for index credits tied to index performance while providing a measure of protection from certain market losses. |

| Variable annuity |

Highest level of risk |

Your money is invested directly in the market. Variable annuities offer the highest growth potential of any of the products on the annuity spectrum, but they also leave you fully exposed to market loss. |

How guaranteed income can support retirement confidence

Economic repercussions have led many people to rethink their appetite for risk and whether their financial strategy still meets their goals. This may be the time to talk with a financial professional about ways to help keep your retirement savings better protected, especially in the event of future downturns.

While investments may continue to play an important role in supporting growth and flexibility, guaranteed income solutions can help you plan for everyday expenses, address rising costs and reduce uncertainty around the income you rely on most in retirement.

Want the most from your retirement? Get smarter with Smart Strategies from Athene. Your source for tips, tools and financial solutions that can help you live your best life.

Guarantees provided by annuities are subject to the financial strength of the issuing insurance company. Guaranteed lifetime income is available through annuitization or the purchase of an optional income rider for a charge.

Fixed indexed and registered index-linked annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.

Although fixed indexed annuities offer principal protection from market downturns, the deduction of applicable charges could exceed any interest credited, resulting in the loss of principal.